The issue is not the litre. It is the fiscal operating system.

In early April 2026, the contrast was impossible to ignore.

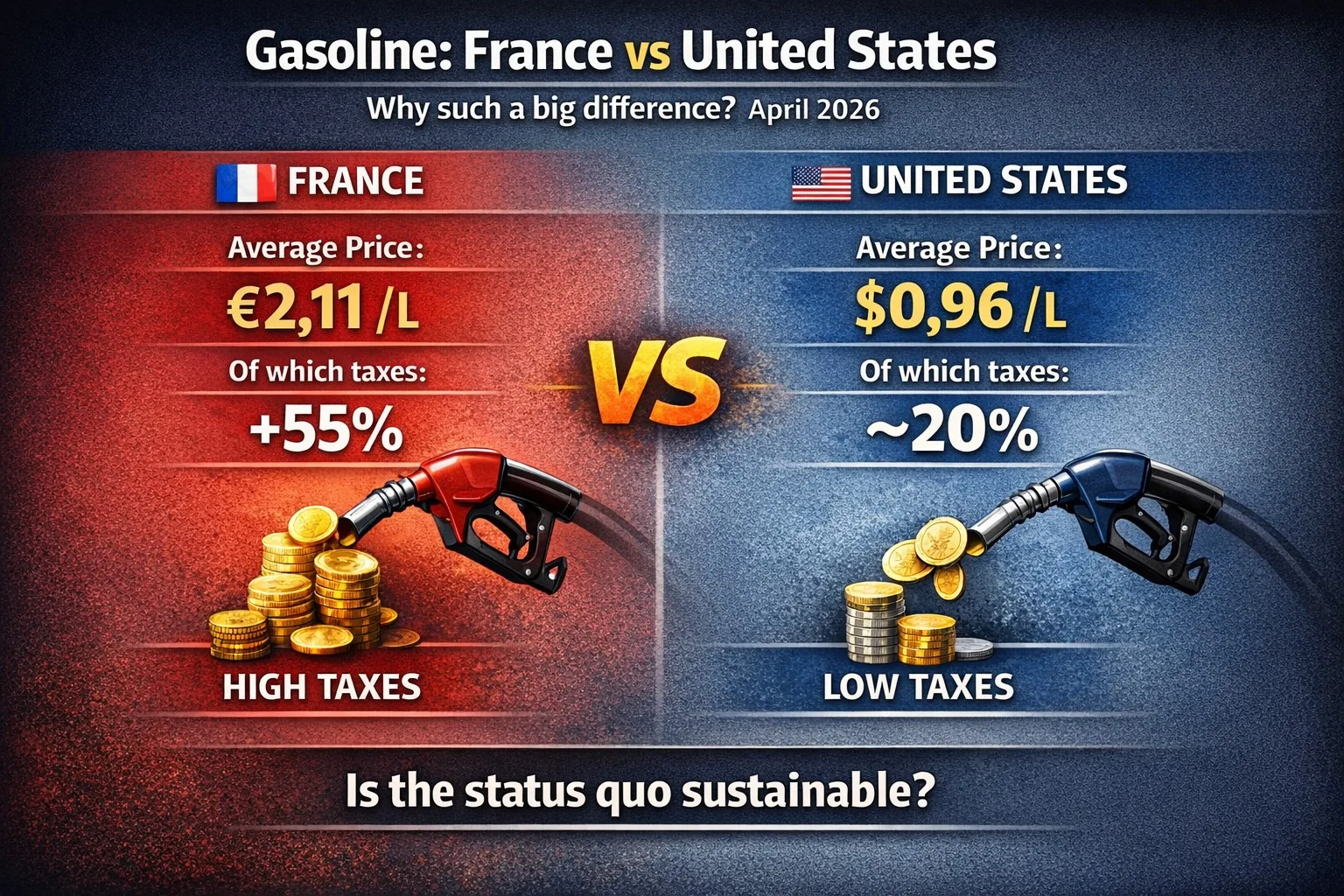

In the United States, regular gasoline was around 4.125 dollars per gallon on April 13, 2026, a little over 1.08 dollars per litre. In France, SP95-E10 was around 2.00 euros per litre on the same date. That gap is massive. It says something about crude oil, refining and distribution, but above all it says something about fiscal philosophy. (AAA, Roole, TF1 Info)

In the United States, gasoline taxation remains relatively moderate compared with the final pump price. The EIA notes that the federal gasoline tax is 18.4 cents per gallon, while average state taxes and fees stood at 33.5 cents per gallon as of January 1, 2026. Even stacked together, that remains far below the French burden. (EIA, EIA)

In France, fuel has become a fully fiscal object. Excise duties apply first, then VAT is levied on the product, including the tax itself. Public schedules confirm the structural weight of fuel taxation. And on February 27, 2026, before the latest geopolitical spike, about 55% of the SP95-E10 pump price already came from taxes according to figures relayed from Ufip. (French Ministry for Ecological Transition, Le Parisien, Fipeco)

This is the core point: the difference between France and the United States is not explained by taxes alone, but taxes are one of the heaviest and most persistent drivers of the gap. Treating that reality as a simple budgetary habit means maintaining the illusion of strategy. (EIA, French Ministry for Ecological Transition)

Status quo bias at the pump

In my book, chapter 6, I explain how status quo bias paralyses organisations.

Here, it does not freeze a management committee.

It freezes political imagination.

Fuel keeps being taxed the way it always has been taxed because the system already exists, because it already generates revenue, because it is administratively convenient, because it avoids opening a more demanding debate.

That is the hidden comfort of the status quo: it postpones thinking.

But a tax that lasts is not automatically an intelligent tax.

An old tax is not a strategy.

A profitable tax is not a mobility policy.

France has loaded too many functions onto the same litre: funding the state, correcting externalities, pushing the transition, shaping behaviour, preserving social acceptability, managing territorial inequalities, calming public anger and balancing the budget. When one instrument is asked to do everything, the result is opacity, rigidity and political flammability.

Fuel has become an emotional spreadsheet.

Every increase replays the same scene.

Every international crisis exposes the same fragility.

Every government rediscovers the same dead end.

And every driver feels they are paying for a strategy that is never clearly explained.

Taxing the past does not build the future

The problem is not taxation itself.

Every modern society taxes.

The problem is taxing a base inherited from an old world as if it could still carry the architecture of a new one on its own.

Twenty-first-century mobility no longer resembles the world for which this tax logic was designed.

Uses are fragmenting.

Powertrains are diversifying.

Territories are living incompatible realities.

Electric vehicles are progressing, but unevenly.

Alternatives do not exist everywhere.

Remote work changes some flows, while other people remain locked into mandatory travel.

And in that landscape, the same fiscal logic keeps falling like an administrative hammer.

This is where immobility becomes more expensive than reform.

When a system can no longer adapt to the diversity of reality, it manufactures injustice, then mistrust, then anger.

What would a twenty-first-century mobility tax system look like?

Not a simple increase.

Not a simple cut.

Not another technocratic gadget.

A credible mobility tax model would need at least five qualities.

1. Readable

Citizens should understand what they are paying, why they are paying it and what it is funding.

Today, too many people see only a final price, not the architecture behind it. Opaque taxation destroys trust before it delivers policy outcomes.

2. Differentiated

The same fiscal framework cannot treat a well-served urban professional, a rural craft business, a car-dependent suburban family and a company with existing logistics alternatives in exactly the same way.

Mechanical equality often produces concrete injustice.

3. Dynamic

A modern tax system should integrate income levels, actual mobility patterns, dependence on the car, the real availability of alternatives and transition goals.

In other words: leave the uniform model, move into the adaptive model.

4. Reversible

When international prices surge, the system should be able to cushion quickly.

When tensions ease, it should return to coherence without permanent improvisation.

The state cannot demand flexibility from citizens while reserving inertia for itself.

5. Strategic

Useful taxation does not merely fill a treasury line.

It organises a shift.

It prepares tomorrow’s behaviours.

It supports investment, equipment, infrastructure, relocation of solutions and the reduction of forced dependency.

The issue is not gasoline. It is our ability to redesign the rules.

The countries that matter tomorrow will not simply be those that tax harder or softer.

They will be those that manage to escape inherited fiscal reflexes and build a full mobility logic instead.

A logic connecting energy, territory, work, infrastructure, technology, climate and social fairness.

Today, France often looks as if it is managing fuel as a yield line.

That is the real problem.

When a country treats mobility as a rent stream, it slows its own transformation.

When it thinks of mobility as a system, it gives itself a chance to become strategic again.

Fuel is therefore not only a purchasing-power issue.

It is a test of public lucidity.

A measure of political creativity.

A mirror of our ability to move beyond a framework that has become too narrow.

Defending the fuel status quo means protecting a recipe.

Reinventing mobility taxation means finally choosing a direction.

References

(AAA) = https://gasprices.aaa.com

(EIA – Factors affecting gasoline prices) = https://www.eia.gov/energyexplained/gasoline/factors-affecting-gasoline-prices.php

(EIA – State taxes and fees on motor gasoline) = https://www.eia.gov/todayinenergy/detail.php?id=67165

(Official French fuel price website) = https://www.prix-carburants.gouv.fr

(French Ministry for Ecological Transition – 2025 Energy Tax Guide) = https://www.ecologie.gouv.fr/sites/default/files/documents/Guide%202025%20sur%20la%20fiscalit%C3%A9%20des%20%C3%A9nergies.pdf

(Roole) = https://media.roole.fr/quotidien/au-volant/prix-des-carburants-voici-les-tarifs-en-france-ce-lundi-13-avril-2026

(TF1 Info) = https://www.tf1info.fr/economie/carburant-les-prix-a-la-pompe-ont-baisse-de-seulement-1-centime-d-euro-en-moyenne-depuis-le-cessez-le-feu-2435703.html

(Le Parisien) = https://www.leparisien.fr/economie/impots-taxes-marche-voici-comment-se-decompose-le-prix-dun-litre-de-carburant-09-03-2026-ODT33AWMSNCYJHTOV3SDVUG5KY.php

(Fipeco) = https://www.fipeco.fr/fiche/Les-taxes-sur-les-carburants